In the summer, McKinsey posted the findings from a study looking at how US consumer preferences for online vs in store shopping were evolving, as a result of the Covid-19 pandemic. The article was written by Tamara Charm, Becca Coggins, Kelsey Robinson and Jamie Wilkie, and is available here.

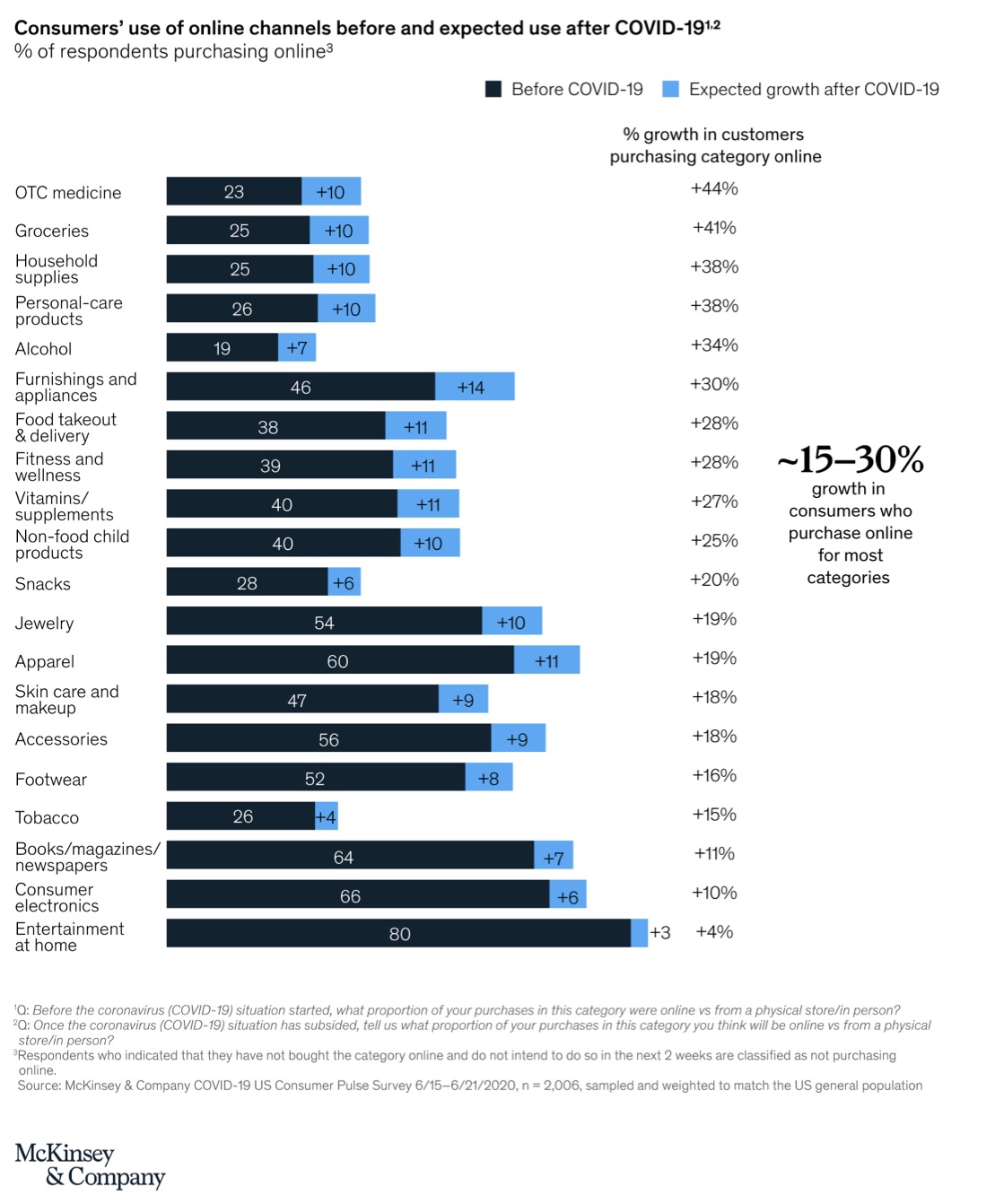

Unsurprisingly, Charm and colleagues found that online shopping had increased across many categories, both for essential items such as medication or groceries, and for non-essential ones such as clothing or entertainment. Moreover, they found that many consumers intended to continue shopping online, particularly for essential items, as illustrated in Figure 1:

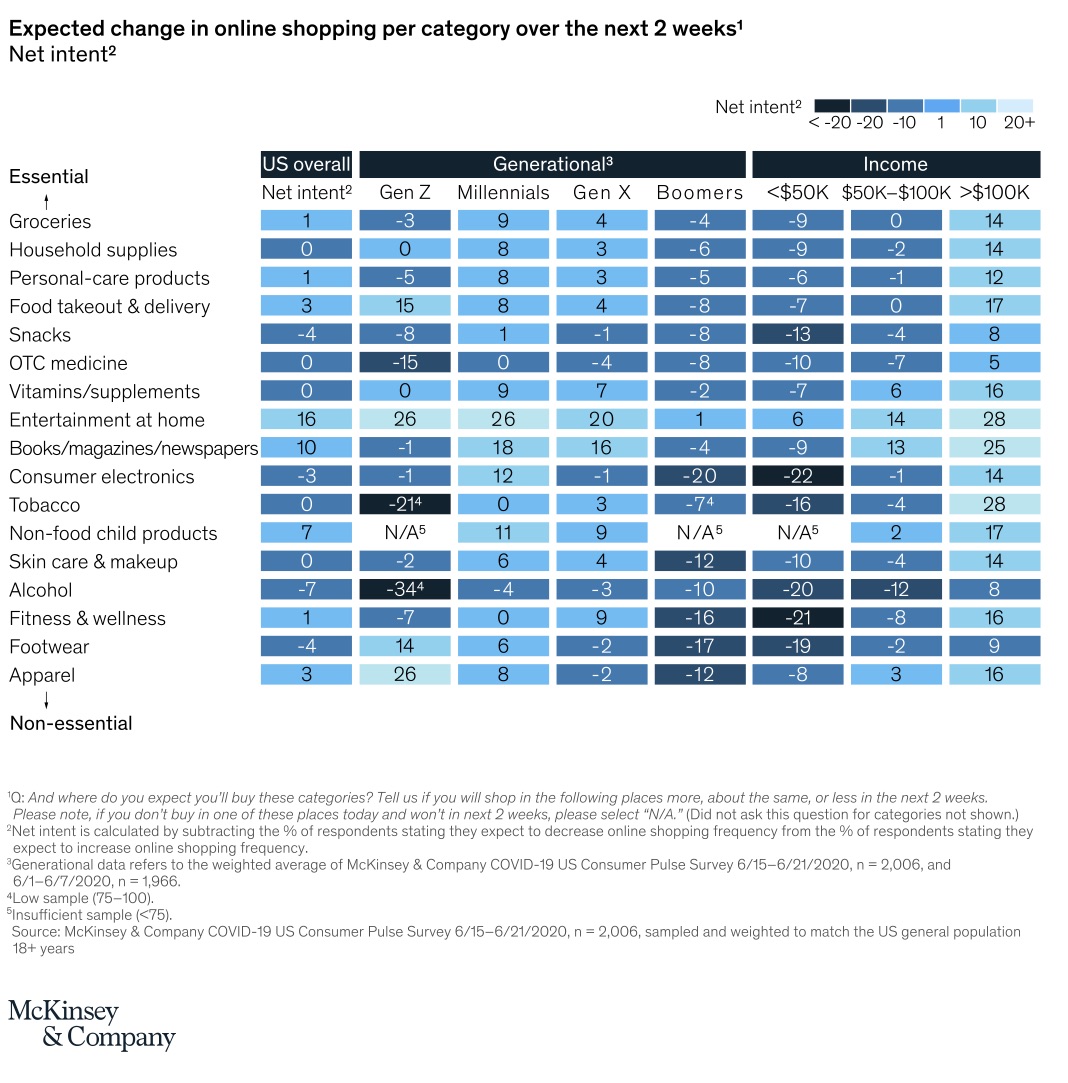

And while there are some differences across age cohorts and income levels (see Figure 2), it looks like adoption of online shopping is here to stay.

Thus, it looks like high street retailers will need to work (even) hard(er) to attract and retain shoppers. But, what should they focus on?

In an article recently published in MIT Sloan Management Review, Jonathan Knowles, Patrick Lynch, Russell Baris and Richard Ettenson report on findings from a research project looking at the motivations of US high street shoppers to continue to shop in store, despite the Covid-19 pandemic. The article is entitled “As Stores Reopen, Which Customers Are Most Likely to Return?”, and is available open access, here.

The researchers identified a segment of shoppers who were very unlikely to return to physical stores. These reluctant shoppers “were never ones to be excited about in-person shopping, even when there wasn’t a pandemic. (…) for them, shopping was and always will be a chore — convenience and simplicity are the main drivers that keep them coming back. To the extent that they have adapted to online shopping, reluctant shoppers are among the least likely to return to stores.”

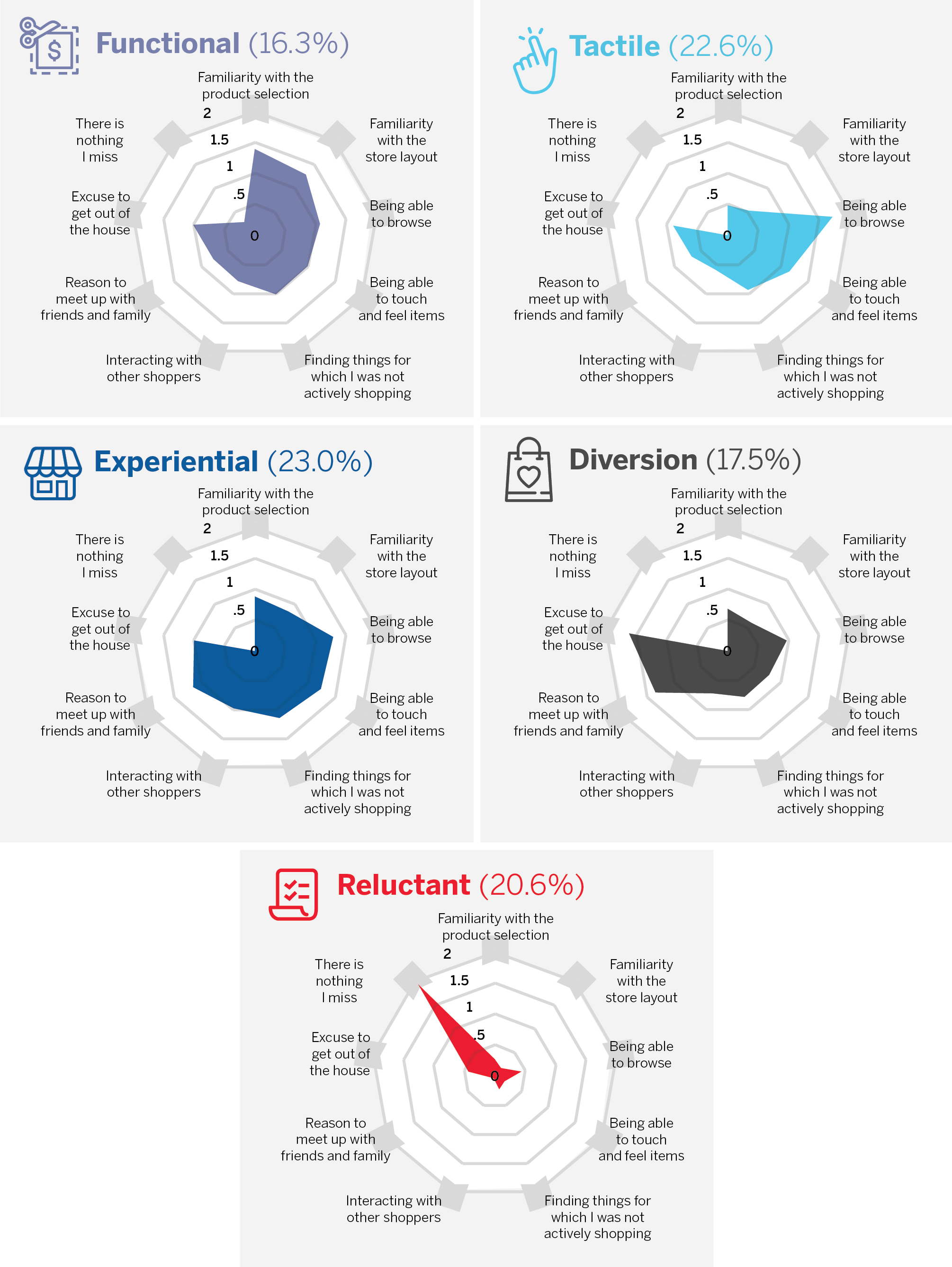

The team also identified four other segments for whom visiting a physical store had clear advantages (Figure 3). They are:

“Functional shoppers are willing to return in-person to retail environments where they are already familiar with the layout and range of products offered. However, they remain concerned about health risks and won’t be going out without their hand sanitizer. This segment also values the experience of coming across new items and interacting with other shoppers, as long as the store has good safety protocols in place. They are keen to try something new, especially if it comes with a discounted price tag.

Tactile shoppers have been bored at home and are eager to hit the stores once they perceive there’s a relatively low health risk during the pandemic. They feel lucky to have kept their jobs but have overdosed on Zoom calls and Netflix and now are excited to get away from the internet browser and back to in-person browsing. When they are finally able to visit their favo(u)rite retailers, they will be thrilled to actually touch items (assuming it is allowed) that they have previewed online and will be open to trying new brands if products feel as good in real life as they looked on screen. Tactile shoppers have high standards, though, and will not return as customers if the experience is less than great.

Experiential shoppers aren’t at the store just to check off items on a shopping list. For this consumer segment, a shopping trip is an event in itself, offering the promise of novelty and the joy of finding something they weren’t actively looking for, with the added opportunity to bring a friend along for the experience. They are especially responsive to brand recommendations from people they trust and always keep an eye out for items they can recommend to others.

Diversion shoppers are eager for the excuse to get out of the house and were among the most excited about stores reopening — a little retail therapy is what they need to end the monotony of lockdown. A price discount might persuade a diversion shopper to try a new brand, and they’ll buy again if they like their purchase but won’t be chatting much to their friends about it. Diversion shoppers can take or leave the social aspect of shopping.” (Source)

In addition, both the McKinsey (Charm et al) and the MIT (Knowles et al) articles report that a significant proportion of customers tried new brands during the pandemic – 36% on Charm et al article; up to 60% on the Knowles et al one.

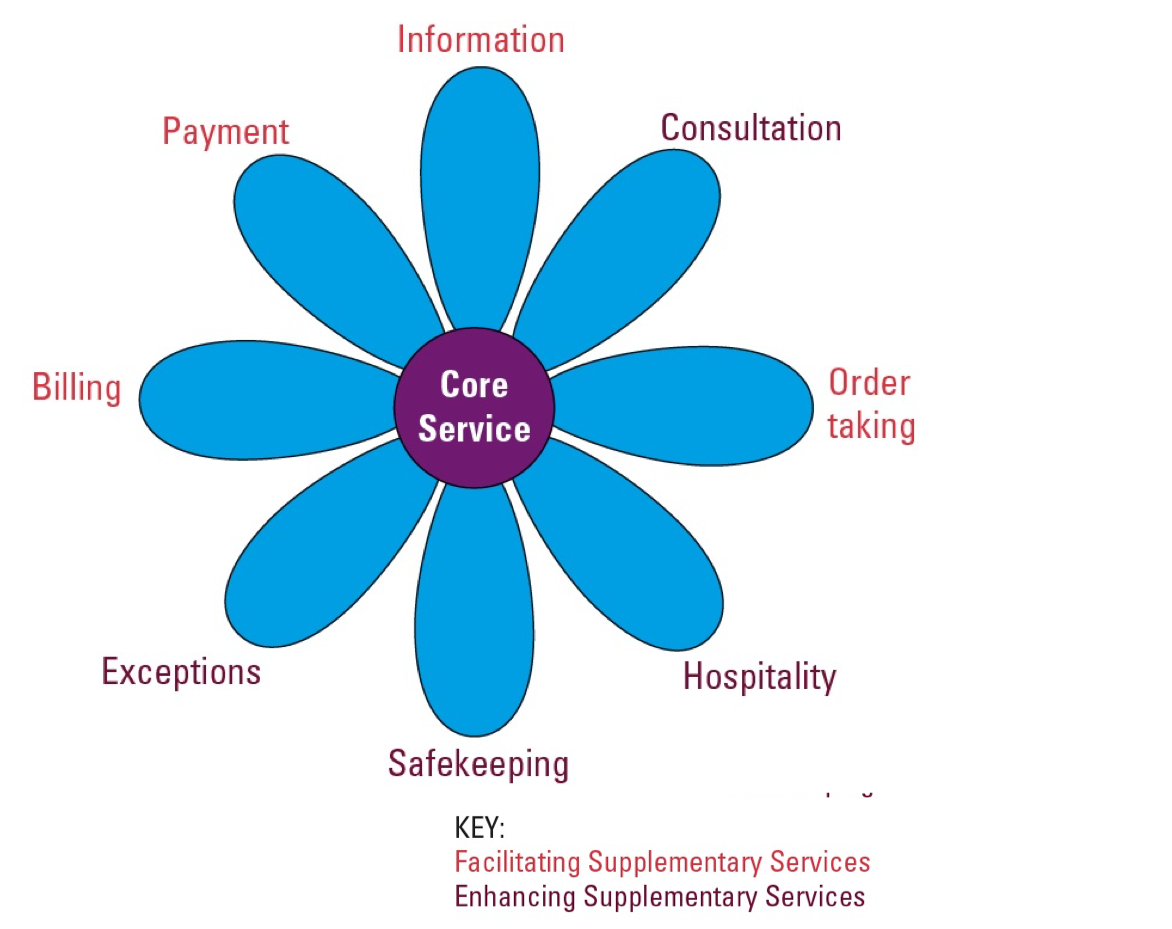

Based on these observations, both studies recommend that brands should ensure product availability and convenience. The Covid-19 pandemic means that online shopping scores very high on the safekeeping dimension of supplementary services (see Figure 4). In some industries, it could also score higher than high street shopping on the information and order taking dimensions, due to the customer reviews available and the convenience of ordering online. Though, for certain products and customers, as shown in the Knowles et al study, physical retail stores are better for information due to the ability to see and try the product, or compare it with other options. Some physical stores may also score better than their online counterparts on the order taking front – for instance, during the UK lockdown, it was sometimes extremely difficult to even access supermarkets’ websites, let alone secure a delivery slot.

The Knowles et al study also recommends a focus on the entertainment and social value of in-store shopping. These suggestions are tapping into the hospitality aspect of supplementary services, making customers feel welcome, and delivering emotional value. This is quite a challenge, when everybody is wearing a mask, and there are so many constraints on customers’ behaviour in the store (e.g., keeping a certain distance from other persons).

To these recommendations, I would add another one. Consultation services. Retailers can add value to in store retail customers by offering advice and making recommendations that help solve the customer’s problem. For instance, I like to stop by my local COOK (as opposed to ordering online) because they always give me good suggestions for foodie gifts, or for how to combine certain mains, side dishes and desserts for guests with dietary restrictions (not that we will be hosting anyone, any time soon).

The bottom line is that the future is looking gloomy for high street retailers. However, this is also an opportunity to move away from price competition, and to focus on other aspects of service that physical stores and their staff can do really well.

Did you change shopping patterns, as a result of Covid-19? What keeps you going to physical stores?

After reading the McKinsey post, I realized how my own shopping habits shifted too. I submitted a one-time Kroger Feedback at http://www.kroger.com/feedback using my Kroger customer card, and surprisingly earned 50 bonus Fuel Points. Kroger supermarket still makes in-store shopping rewarding—especially for loyal buyers in Ohio like myself.

LikeLike

Kroger being a US world largest retailer, uses customer surveys often to make assumptions about their food products and services, and estimate how satisfied their customers are. The Survey are collected through http://www.kroger.com/feedback to collects opinions, preferences, and experiences from grocery store customers.

LikeLike