Customers differ in the value that they generate for the firm. Some generate revenues well above the costs of serving them. Others, a net loss. Others, still, are outright disruptive, engaging in behaviour that is very costly to the firm. Accordingly, the marketing literature (particularly, in the field of relationship marketing) recommends that managers should concentrate marketing resources on acquiring and retaining ‘good’ customers.

But what makes a customer ‘good’?

Conceptually, a good customer is one whose expected revenue streams exceed the expected costs of acquiring, serving and keeping them. So, finding these customers requires predicting their future behaviour.

In the case of personal credit, for instance, a good customer is one who will repay their debt. As repayment takes place several years after the loan is granted, lenders collect data about various aspects of the applicant’s identity and behaviour, to infer their ‘credit worthiness’ – such as, the applicant’s credit history; their occupation; length of employment; credit rating; marital status; bank account; neighbourhood; collateral; length of residence; income; and gender.

However, that is not the whole story.

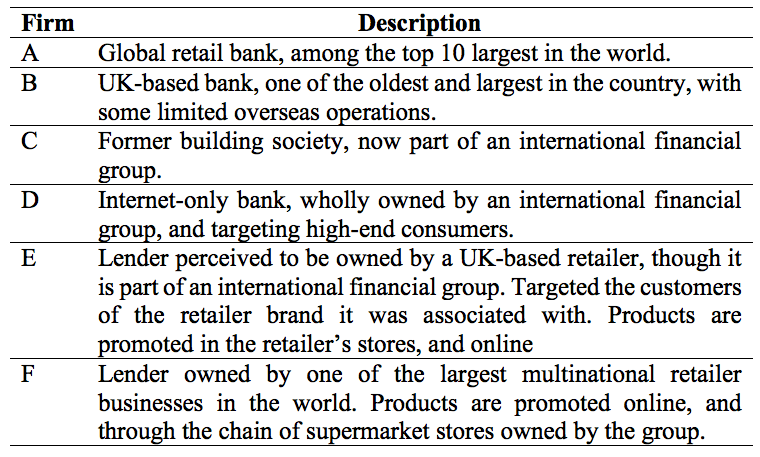

Professor Sally Dibb and I have long been interested in how firms decide which customers to promote or demote. As part of that research agenda, we studied lending practices in the UK, examining how the definition of a good customer (in this case, ‘good’ = credit worthy customer) varied across different institutions and over time. Specifically, we followed lending practices at six retail banks (see table 1), over a period of 10 years, from 2003 to 2013.

We found that, at the height of the credit crunch crisis of 2008, which triggered an economic recession in the UK, it was much more difficult for loan applicants to obtain credit because many mainstream creditors had changed their lending criteria and practices.

For instance, all six case studies withdrew certain products from the market, particularly 100% mortgages and secured loans that allowed homeowners to borrow money against equity held in their properties. Most lenders closed credit lines, or stopped taking new customers altogether. And all but one lender in our sample said that they had raised the lending threshold levels because of:

- Changes in Strategic objectives (e.g., desired market share in a particular market);

- Lower willingness to take risks;

- Some lenders faced cash flow problems.

For the remaining products, in five out of the six case studies, loan applicants had to obtain higher credit scores to be granted a loan in 2008, than in 2003.

Furthermore, our analysis showed that some of the changes in lending practice brought in 2008, were still in place in 2013.

That is, customers who would have been deemed ‘good’ in 2003 saw their status change by 2008 or 2013, not because of a change in their personal circumstance or behaviours, but because of changes in the supply side. Yet, supply side factors are not part of the widely accepted and used definitions of customer quality.

Our study documented how firm-related factors such as strategic targets, stakeholder structure, capitalisation structure, or risk appetite shape who is and is not credit worthy customer – that is, who is a good customer. This is important from a conceptual perspective, because it shows that ‘customer quality’ is not only subjective (varying from firm to firm) but also extrinsic to the customer. The definition(s) of customer quality and value do not reflect this reality.

Our study also showed that the young, migrants and socially excluded groups were at risk of further marginalisation during the recession, while customers not traditionally referred to as ‘vulnerable’, found themselves in financial difficulties in the period under analysis. This is important from a practical perspective because access to credit allows consumers to acquire products that are essential for their well-being and increases their confidence and ability to participate in society. While there are various governmental and charitable initiatives tackling financial vulnerability, they tend to focus on personal factors, whereas our study showed that the context determines vulnerability.

You can read more about this study here (50 free downloads available).

2 thoughts on “What makes a customer ‘good’?”