When the UK went into lockdown, the process of selling our flat stalled, as both the buyer and ourselves are facing various practical barriers to execute the sale.

We are not the only ones, of course. Even before the lockdown, house sales were falling (40% fewer enquiries and 15% fewer sales agreed, according to property website Zoopla); and it is now predicted that the next quarter will see a reduction in sales of, at least, 60%. And, to make matters worse, mortgage lenders have dramatically reduced their mortgage offering. This is due to three main forces.

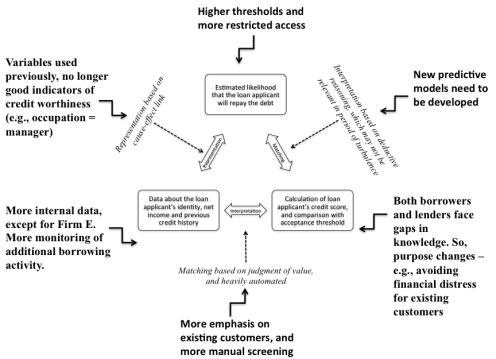

First, surveyors can’t visit properties due to the lockdown, meaning that they can’t fully assess the value of a property. As a result, they are reducing the loan to value ratio to as little as 60% of the property value (down from 90%, in some cases).

Second, some staff in banks are isolating, others are furloughed, and the remaining ones are dealing with a spike in enquiries about mortgage payment holidays, meaning that lenders have limited staff availability. As a result, it is taking longer for lenders to process applications.

Third, the uncertainty regarding the duration of this crisis makes it difficult to predict its economic impact, meaning that it is difficult for lenders to predict the affordability of the loans several months down the line. As a result, many are only considering applications from existing customers.

The cumulative impact of these three trends is that it is very difficult for house buyers to secure a loan, especially if they are new to the market and if they have little equity. And, for the others, there are fewer options and it takes longer to secure a loan.

If this state of affairs sounds familiar, it’s because it is! Fewer loans, lower loan to value ratios, a focus on existing customers, and delays in processing applications are exactly what we witnessed during the 2008-09 crisis. Twelve years ago, there was no deadly virus around, and social distancing was not part of our vocabulary. Instead, the UK (like other economies) was in the grips of a major financial and economic crisis, triggered by the ‘credit crunch’ of 2007. Many – if not all – financial institutions were finding it very difficult to raise money in the secondary market and, as a result, they had less money available to lend. That’s not the situation, now. There is money available to lenders, at least for now. However, for the three reasons listed above, we are still witnessing a reduction in the supply of loans, just like we witnessed 12 years ago.

Given the similarity in response from lenders today vs. 2008/09, we can look at what happened, then, to predict the likely impact of this response on would-be borrowers.

I conducted a longitudinal study of the customer screening and lending practices of six UK lenders, to analyse lenders’ response during the 2008-09 crisis, and its impact on consumer vulnerability. This study covered a period of 10 years, from 2003 to 2013 (So, roughly, 5 years before and 5 years after the onset of the recession). The findings from the study are reported in this paper, published in the Journal of Marketing Management; and discussed in this blog post.

Through my analysis, I found that the withdrawal of high loan to value products, and the focus on existing customers, at the height of the crisis, had a disproportionate impact on certain types of customers. Those most likely to suffer were the young, migrants and those that had stayed away from the mainstream financial services for social or cultural reasons (e.g., stay at home mothers). These customers either had no access to the market at all, or they had fewer and more expensive options to choose from, which was likely to accentuate their financial problems. That is, the borrowers that were already at a disadvantage, facing higher living costs and struggling to access the market, were now also facing additional practical and emotional hurdles, as a result of not being able to secure credit from mainstream lenders.

In addition, the delays in processing applications created cash flow problems for some customers. Some people lost deposits, others missed payments and were charged penalties, still others had to get short term loans at higher rates. Their cost of living increased. Such delays can also be a source of distress and feelings of powerlessness.

Most significantly, 5 years later, some of those “short-term reactions” to the credit crunch were still in place. For instance, some lending products targeted at the more financially vulnerable were never reintroduced. So, the temporary market disruptions created by the credit crunch had long term implications for the most vulnerable customers.

Likewise, the impact of the immediate reaction to Covid19, by mortgage lenders, is likely to be felt by buyers, sellers and intermediaries long after we leave lockdown, drop the face masks, and forget to keep 2 metres away from other people.

Has the mortgage lockdown impacted you?

Very interesting, although it makes depressing reading. We both have moving projects held up by serious uncertainty in the housing market. If 2019 prices drop it could be a serious problem for us. The main thing, though, is to understand what might happen, so thank you for this. If lenders revert to what they did in 2008 we need to re-think our strategy.

LikeLiked by 1 person