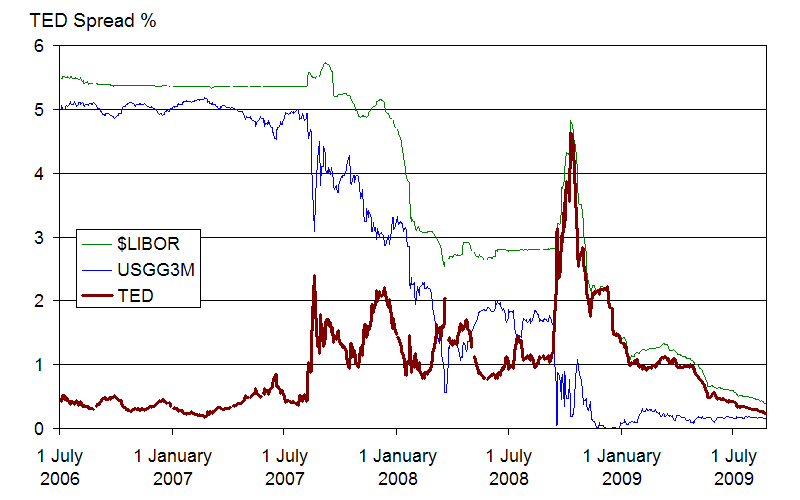

Ten years ago, the UK was in the grips of a major financial and economic crisis, triggered by the ‘credit crunch’ experienced in the previous year (1). Major financial institutions like Northern Rock or Lehman Brothers went bankrupt, others like the Royal Bank of Scotland required government intervention to stay afloat, and most – if not all – were finding it very difficult to raise money.

As a result, banks had less money available to lend, and made changes to their practices. But how were these changes reflected in how credit decisions were made and, ultimately, how did these changes impact on consumers?

To answer these questions, I conducted longitudinal case studies of the customer screening practices of six UK lenders (see table 1), covering a period of 10 years (from 2003 to 2013).

Table 1. Overview of the six case studies

| Bank | Description |

| A | Global retail bank, among the top 10 largest in the world. |

| B | UK-based bank, one of the oldest and largest in the country, with some limited overseas operations. |

| C | Former building society, now part of an international financial group. |

| D | Internet-only bank, wholly owned by an international financial group, and targeting high-end consumers. |

| E | Lender perceived to be owned by a UK-based retailer, though it is part of an international financial group. Targeted the customers of the retailer brand it was associated with. Products are promoted in the retailer’s stores, and online |

| F | Lender owned by one of the largest multinational retailer businesses in the world. Products are promoted online, and through the chain of supermarket stores owned by the group. |

The findings from the analysis of the interview data, brochures, financial statements, analyst reports and many other documents collected for this study have been reported in a paper published here, which was co-authored with Professor Sally Dibb. A pre-print, open access version of the paper is available here.

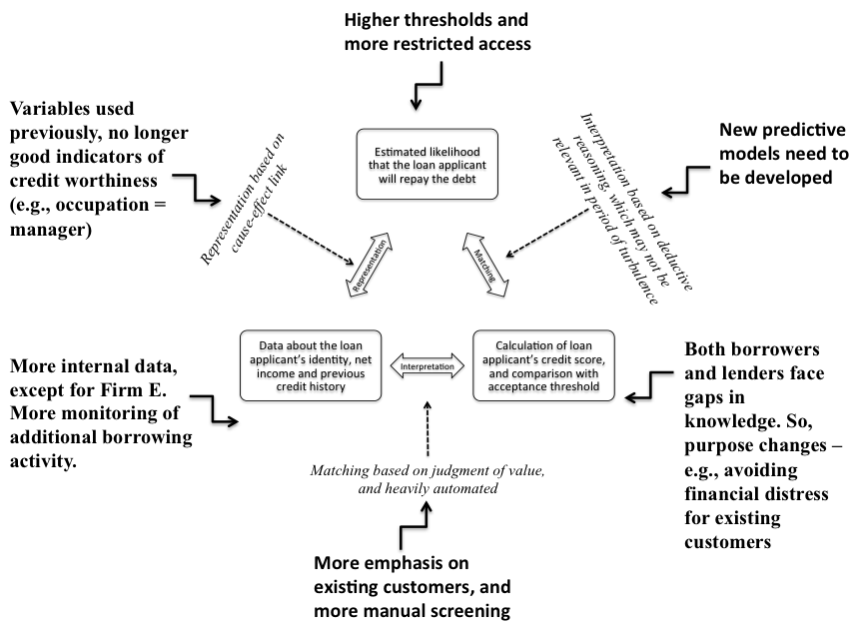

One of the key findings from this investigation was that several lenders turned inwards when assessing lending risk, privileging internal data about customers, lending performance, etc… As a result, new consumers, or those with few existing products with a particular lender, were disadvantaged when applying for a loan, vs. others with many products with that same lender.

We also found that lenders removed various products from the market such as unsecured loans or 100% funding. These products are particularly relevant for new borrowers, who have limited savings and/or no assets.

These two factors combined mean that certain groups of customers found it very difficult to get access to credit. For instance, the young, migrants and those that had stayed away from the mainstream financial services for social or cultural reasons (e.g., stay at home mothers), would have very limited options to choose from. The resulting financial exclusion would have pushed these customers into high cost alternatives such as pay day loans, credit card debt and so on, possibly deepening their social exclusion.

But it wasn’t just the “traditionally vulnerable” that would have struggled. Our analysis showed that, in the aftermath of the credit crunch, lenders adopted a narrower definition of what constituted a good borrower. On the one hand, variables which had been previously used as indicators of good credit quality (e.g., managerial jobs) lost their relevance in this period. On the other hand, lenders raised the hurdle to be met when applying for a loan. For instance, in five out of the six lenders investigated, loan applicants had to obtain higher credit scores to secure a loan, than would have been the case before the 2008 crisis. That is, not only did prospective borrowers have access to fewer choices, but they also faced shifting and more stringent requirements.

Another interesting finding was that lenders increased the proportion of loan applications that went through manual screening for approval. Manual screening is associated with lower default rates than automated screening and, so, it is a sensible option for lenders to follow, in order to reduce their exposure to bad debt. However, manual screening significantly slowed down the process of reviewing and approving applications, meaning that it took longer for applicants to obtain a loan. This delay created cash flow problems for some customers, which they dealt with by using high cost credit forms such as credit card debt, or pay day loans.

In summary, the recession put the young, migrants and socially excluded groups at risk of further marginalisation; while customers not traditionally considered vulnerable, found themselves in financial difficulties. These groups’ vulnerability resulted from factors completely outside of their control. It was the combination of firm-related factors – like reduce risk appetite, fewer products to choose from, more stringent requirements and slower screening processes – which, in the end, determined who was and was not deemed a “good” customer.

A somber reflection, given the cyclical nature of economic recessions, the long-term consequences of temporary decisions, and the growing evidence that the private sector is neither likely nor able to take sole responsibility for addressing financial exclusion.

(1) This piece by the BBC provides a good explanation of the link between the sub-prime lending problems, the resulting credit crunch of 2007, and the subsequent economic crisis

4 thoughts on “How did the 2008 financial crisis impact on financial exclusion?”