Last week, the news broke that Admiral car insurance planned to launch a new product aimed at new drivers, firstcarquote, whereby policy holders could get rebates on their annual premium, based on their social media activity.

Last week, the news broke that Admiral car insurance planned to launch a new product aimed at new drivers, firstcarquote, whereby policy holders could get rebates on their annual premium, based on their social media activity.

The Guardian reported that:

Admiral Insurance will analyse the Facebook accounts of first-time car owners to look for personality traits that are linked to safe driving. For example, individuals who are identified as conscientious and well-organised will score well. The insurer will examine posts and likes by the Facebook user, although not photos, looking for habits that research shows are linked to these traits. These include writing in short concrete sentences, using lists, and arranging to meet friends at a set time and place, rather than just “tonight”.

In contrast, evidence that the Facebook user might be overconfident – such as the use of exclamation marks and the frequent use of “always” or “never” rather than “maybe” – will count against them.

(…)

The scheme is based around algorithms that have been developed by Admiral. The technology uses social data to make a personality assessment and then, judging against real claims data, analyse the risk of insuring the driver.

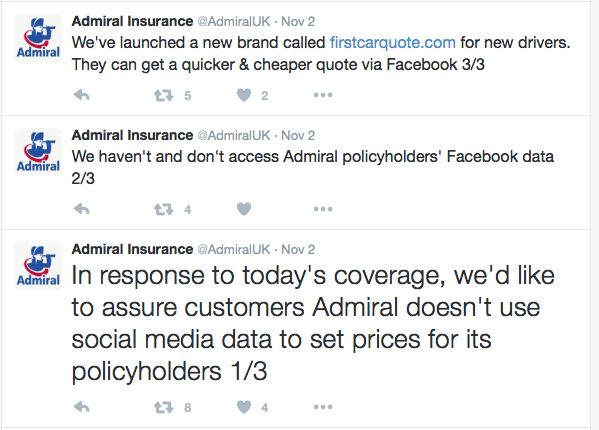

The news attracted considerable press and social media attention. The move was labelled as intrusive, and a threat to consumers’ privacy, forcing the company to clarify that they were not (yet) using Facebook data to set prices:

And, it seems that they will not be able to do it in the future, either, because Facebook has moved in to block their plans, stating that it contravened point 3.15 of their policy for platform developers*:

But the underlying question in this story was: Can the automated analysis of our words and actions, online, be a good predictor of our psychological traits and of our behaviours?

Well, it turns out, that yes, they do. Very well, in fact.

A study by Michal Kosinski, David Stillwell and Thore Graepel had already showed that computer analysis of our Facebook likes can predict our personality traits (as well as other very sensitive things like sexual orientation, political views, or the use of addictive substances).

But another study by Wu Youyou, Michal Kosinski, and David Stillwell went further and showed that, by analysing our Facebook likes, computers are able to predict our personality and behaviours better than our friends and close relatives.

Digital footprints are excellent predictors of our personality because, essentially, there are a lot of data points available to be processed – all of them, time and location stamped, and linked (or linkable) to a single person.

So, the answer to the question above is a clear, resounding yes.

But that does not mean that companies should do it, of course. As discussed in our book, The Dark Side of CRM**, we do not like when other people (and firms) know things about us that we feel should not be common knowledge. We feel that our personal space has been invaded, and instinctively pull away from that person / company / relationship. We also like to think of ourselves as unique, independent individuals; and resist the idea that we are easily pigeonholed, and predictable. These are deeply ingrained feelings and reactions, so it is not a good idea for marketers to go against them.

An alternative (and, in my view much better) approach is that followed by MAPFRE Malta.

Like Admiral, MAPFRE developed a product specifically for new drivers, Motormax. And like Admiral, MAPFRE wanted to reward careful and sensible young drivers. But, unlike Admiral, MAPFRE focused on monitoring actual driving behaviour. How?

With permission from the driver, MAPFRE installs a small*** Internet of Things device on the car, which monitors driving behaviour. Those drivers that:

- Drive within the speed limit (this is monitored on an area by area basis);

- Do not drive between the hours of midnight and 5 am;

- Drive less than a certain distance and/or amount of time per month

receive a rebate up to 40% on their premium.

In both cases, there is surveillance and monitoring. But, in my view, MAPFRE’s approach is superior because there is a direct link between the behaviour being monitored and the desired outcome and, so, it is easier for consumers to accept it. Also, very importantly, there is less room for unintended and unanticipated consequences of data misuse.

What was your reaction to the Admiral news?

* A move that attracted the praise of privacy-protection groups (a first for Facebook)!

** First chapter available here, free

*** About the size of half of thumb

One thought on “From Facebook likes and Internet of Things, to insurance premiums”